Indexed Universal Life (IUL) and Whole Life Insurance: Which One is Right for You?

Choosing the right life insurance policy is one of the most critical financial decisions you’ll make. With so many options available, Indexed Universal Life (IUL) and Whole Life Insurance are two popular choices for individuals looking for long-term protection and wealth-building potential. But which one is the right fit for you?

At Prosperity Edge Consulting, we help clients navigate the complexities of life insurance to ensure they choose a policy that aligns with their financial goals. In this guide, we break down the key differences between IUL and Whole Life Insurance, their benefits, drawbacks, and when to choose each policy.

What is Indexed Universal Life (IUL)?

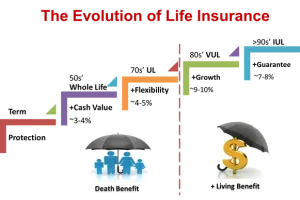

Indexed Universal Life (IUL) is a type of permanent life insurance that offers both a death benefit and a cash value component that grows based on market performance. Unlike Whole Life Insurance, which provides a fixed interest rate, IUL links cash value growth to a stock market index, such as the S&P 500.

What is Whole Life Insurance?

Whole Life Insurance is a traditional permanent life insurance policy that provides a guaranteed death benefit, fixed premium, and predictable cash value growth. The cash value grows at a fixed interest rate set by the insurance company and is not tied to market performance.

Key Differences Between IUL and Whole Life Insurance

| Feature | Indexed Universal Life (IUL) | Whole Life Insurance |

|---|---|---|

| Premiums | Flexible premiums | Fixed premiums |

| Cash Value Growth | Market-linked (S&P 500, etc.) | Guaranteed fixed rate |

| Death Benefit | Adjustable | Guaranteed |

| Risk Level | Moderate (market exposure) | Low (stable, predictable) |

| Loan/Withdrawal Flexibility | High | Moderate |

| Ideal For | Growth potential, tax-free withdrawals | Stability, guaranteed returns |

Pros and Cons of Indexed Universal Life (IUL)

✅ Pros of IUL

- Higher Growth Potential: Cash value accumulates based on market performance.

- Flexible Premiums: You can adjust payments as needed.

- Tax-Free Retirement Income: Withdrawals and loans can be taken tax-free.

- Adjustable Death Benefit: Policyholders can modify coverage as their financial situation changes.

❌ Cons of IUL

- Market Risk: While IULs offer growth potential, they also expose policyholders to market downturns.

- Complexity: More difficult to understand compared to Whole Life Insurance.

- Fees & Caps: Earnings may be capped, and fees may reduce overall returns.

Pros and Cons of Whole Life Insurance

✅ Pros of Whole Life Insurance

- Guaranteed Growth: Predictable, stable cash value accumulation.

- Fixed Premiums: No unexpected cost increases over time.

- Lifetime Coverage: Permanent coverage with guaranteed death benefit.

- Dividend Payments: Some policies offer dividends that can be reinvested or used for premium payments.

❌ Cons of Whole Life Insurance

- Higher Premiums: Typically more expensive than IUL due to guarantees.

- Lower Growth Potential: Cash value grows at a fixed rate, offering limited upside.

- Less Flexibility: No option to adjust premium payments or investment choices.

When to Choose IUL vs. Whole Life Insurance

Choose IUL If:

✅ You want higher cash accumulation potential.

✅ You prefer flexible premium payments.

✅ You’re comfortable with market-linked returns.

✅ You plan to use the policy for tax-free retirement income.

Choose Whole Life Insurance If:

✅ You value guaranteed returns and stability.

✅ You prefer a fixed premium with no surprises.

✅ You want long-term financial security for your family.

✅ You’re looking for dividends and additional cash flow.

Frequently Asked Questions (FAQs)

Q: Which policy is better for building wealth?

A: If you’re looking for higher growth potential, Indexed Universal Life (IUL) is the better option because it allows cash value accumulation based on market performance. However, Whole Life Insurance provides a stable, guaranteed return with lower risk.

Q: Can I switch from Whole Life to IUL later?

A: Yes, but switching may come with fees, surrender charges, and new underwriting. It’s essential to assess whether the switch aligns with your financial goals.

Q: Can I use IUL or Whole Life Insurance for retirement income?

A: Yes! Both policies allow tax-free loans and withdrawals, but IUL provides greater flexibility and higher potential returns, making it a preferred choice for retirement income strategies.

Q: How do policy loans work for IUL and Whole Life?

A: Policyholders can borrow against the cash value in both types of policies. However, IUL loans may have variable interest rates, while Whole Life loans typically have fixed rates.

Final Thoughts: Which Policy is Right for You?

Both Indexed Universal Life (IUL) and Whole Life Insurance have unique benefits, and the right choice depends on your financial goals, risk tolerance, and coverage needs.

At Prosperity Edge Consulting, we help clients find the perfect life insurance strategy tailored to their long-term wealth-building and protection goals.

➡️ Schedule a free consultation with us today and take the next step toward financial security!

📍 Visit Prosperity Edge Consulting to learn more.

Reference: Prosperity Edge Consulting’s Financial Experts