Indexed Universal Life Insurance (IUL) is a unique financial product that combines the benefits of life insurance with the potential for cash value accumulation linked to market index performance. This dual advantage not only provides a death benefit to your beneficiaries but also offers a strategic avenue for wealth building.

Understanding Indexed Universal Life Insurance.

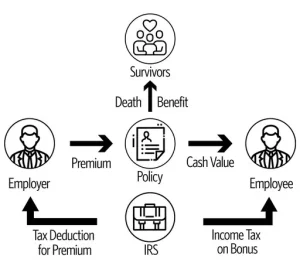

IUL is a type of permanent life insurance that offers flexibility in premium payments and death benefits. A portion of your premium goes towards the cost of insurance, while the remainder contributes to the policy’s cash value. This cash value is credited with interest based on the performance of selected equity indexes, such as the S&P 500 or the Nasdaq-100. It’s important to note that while the cash value growth is linked to these indexes, your money isn’t directly invested in the stock market, providing a layer of protection against market downturns. investopedia.com

The Wealth-Building Potential of Indexed Universal Life Insurance (IUL)

-

Tax-Advantaged Growth: The cash value in an IUL policy grows tax-deferred, meaning you won’t pay taxes on the earnings as they accumulate. This allows your wealth to compound more efficiently over time.

-

Market-Linked Interest: IUL policies credit interest based on the performance of chosen market indexes. This offers the potential for higher returns compared to traditional whole life insurance policies, especially during strong market periods. However, it’s essential to understand that these policies often come with participation rates and caps that can limit the credited interest. investopedia.com

-

Flexible Access to Cash Value: One of the significant advantages of IUL is the ability to access the accumulated cash value through policy loans or withdrawals. These funds can be used for various purposes, such as supplementing retirement income, funding education, or covering unexpected expenses. It’s crucial to manage these withdrawals carefully to maintain the policy’s integrity and death benefit.

-

Protection Against Market Downturns: While IUL policies offer exposure to market gains, they also provide a safety net against losses. Many policies have a guaranteed minimum interest rate, ensuring that your cash value doesn’t decrease due to negative index performance. This feature helps preserve your wealth during market volatility.

Considerations When Choosing an Indexed Universal Life Insurance (IUL Policy)

- Cost of Insurance: As you age, the cost of insurance within the policy can increase, potentially affecting the cash value growth. It’s essential to monitor the policy’s performance and adjust premium payments accordingly.

- Policy Fees and Charges: Be aware of the various fees associated with IUL policies, including administrative fees, surrender charges, and costs related to additional riders. These can impact the overall returns of the policy.

- Cap Rates and Participation Rates: Understand the limitations set by the insurer on the interest credited to your policy. Cap rates limit the maximum interest credited, while participation rates determine the percentage of the index gain credited to your policy.

Is IUL Right for You?

Indexed Universal Life Insurance can be a valuable tool for individuals seeking life insurance coverage with the added benefit of cash value accumulation linked to market performance. However, it’s not suitable for everyone. Those who are risk-averse or prefer guaranteed returns might find traditional whole life insurance more appropriate. It’s advisable to consult with a financial advisor to assess whether an IUL policy aligns with your financial goals and risk tolerance.

In conclusion, Indexed Universal Life Insurance offers a compelling combination of life insurance protection and wealth-building potential. By understanding its features, benefits, and considerations, you can make an informed decision to enhance your financial strategy.

Frequently Asked Questions (FAQs) About Indexed Universal Life Insurance (IUL)

1. How does Indexed Universal Life Insurance (IUL) build wealth over time?

Indexed Universal Life Insurance builds wealth through a cash value component that grows based on market-linked index performance (e.g., S&P 500). Unlike traditional savings accounts, the earnings grow tax-deferred, allowing policyholders to accumulate tax-free wealth over time.

- How does Indexed Universal Life Insurance accumulate wealth?

- Best life insurance policies for tax-free retirement savings

2. Is Indexed Universal Life Insurance a good investment for retirement planning?

IUL can be a valuable tool for retirement planning, offering a tax-free income stream through policy loans and withdrawals. Unlike 401(k)s or IRAs, IUL policies do not have mandatory withdrawal requirements (RMDs), making them a flexible option for retirees.

- Is Indexed Universal Life Insurance good for retirement?

- Best life insurance policy for retirement planning

3. What are the tax advantages of an Indexed Universal Life Insurance policy?

IUL policies offer multiple tax benefits, including:

✅ Tax-deferred growth on cash value accumulation

✅ Tax-free withdrawals (if structured properly)

✅ Tax-free death benefit for beneficiaries

These benefits make IUL a powerful tax-free wealth-building strategy.

- Indexed Universal Life Insurance tax benefits explained

- Tax-free investment options with life insurance

4. Can you lose money in an Indexed Universal Life Insurance policy?

Unlike traditional investments, IUL policies have a downside protection feature, meaning they are shielded from market losses through a guaranteed 0% floor. This means even if the stock market declines, your policy’s cash value will not decrease due to market fluctuations.

- Does Indexed Universal Life Insurance have market risk?

- How safe is Indexed Universal Life Insurance?

5. How does Indexed Universal Life Insurance compare to Whole Life Insurance?

|

Feature |

Indexed Universal Life (IUL) |

Whole Life Insurance |

|

Premium Flexibility |

High |

Low |

|

Cash Value Growth |

Market-linked |

Fixed growth |

|

Risk Protection |

0% floor, no losses |

Guaranteed growth |

|

Wealth-Building Potential |

Higher |

Moderate |

IUL policies offer greater flexibility and higher potential returns compared to Whole Life Insurance, making them a better choice for long-term wealth accumulation.

- Indexed Universal Life vs Whole Life Insurance comparison

- Which is better: IUL or Whole Life Insurance?

6. Who should consider buying an Indexed Universal Life Insurance policy?

An IUL policy is best suited for:

✔ High-income earners looking for tax-free retirement income

✔ Business owners needing a flexible financial planning tool

✔ Parents saving for college tuition with tax-free withdrawals

✔ Investors seeking downside protection with market-linked growth

- Who benefits the most from Indexed Universal Life Insurance?

- Best life insurance policy for high-income earners

7. How do policy loans work in an Indexed Universal Life Insurance policy?

Policyholders can borrow against their IUL cash value through tax-free policy loans. Unlike traditional loans, no credit check or approval is required, and the loan does not have to be repaid as long as the policy remains in force.

- How do tax-free loans work in Indexed Universal Life Insurance?

- Can I use Indexed Universal Life Insurance as a bank?

8. What are the disadvantages of Indexed Universal Life Insurance?

While IUL policies offer many benefits, they also have some drawbacks:

Cap rates on growth – Your returns are limited by a cap set by the insurer.

Policy fees and costs – Administrative and insurance charges can reduce cash value.

Requires long-term commitment – Best suited for individuals with a long-term wealth-building strategy.

- What are the downsides of Indexed Universal Life Insurance?

- Does Indexed Universal Life Insurance have high fees?

9. Can I use Indexed Universal Life Insurance for college funding?

Yes! IUL is a popular strategy for college savings, as it allows parents to accumulate tax-free cash value and withdraw funds without penalties. Unlike 529 Plans, IUL withdrawals do not count against financial aid eligibility.

- Best life insurance policy for college savings

- How to use Indexed Universal Life Insurance for education funding

Ready to unlock the hidden wealth-building potential of Indexed Universal Life Insurance? Speak with an expert today and start securing your financial future

Pingback: How Living Benefits Can Provide Financial Security During Critical Illness | Indexed Universal Life Insurance

Pingback: 5 Myths About Final Expense Insurance You Need to Stop Believing | Get the Facts